The South African Rand kept up to its reputation as a high beta currency in the last quarter of 2022, with USDZAR moving almost 10% from high to low, while the comparable index of EM currencies moved only 6%. This was the quarter when Dollar went through a sizeable correction to its 16 month rally, the trigger coming from the steady moderation in US inflation and the rate hike prospects being sized down by the market, though FED officials remained hawkish. Investors took profit on their Dollar long positions and bought back bonds which had fallen substantially. Even Global stock Index recovered as much as 18% despite recession fears in the background and here too the South African benchmark index outdid by rising by more than 23% from the lows.

MACRO DEVELOPMENTS

TRADE SURPLUS of South Africa is estimated to fall far short of the robust one posted in 2021. Trade surplus for the 11 months to the end of November was R187.8-billion, less than half of the R402-billion recorded over the same period in 2021. But the sizeable fall in oil price is already helping to arrest this trend. In fact, Current Account Deficit as a percentage of GDP has slightly improved from -1.3% to -0.3% as a direct result of trade balance improving in November. The balance of payment was affected by more capital flowing out than what came in.

COMMODITY INFLUENCE: The oil price is losing its lustre in the face of a slowing global economy, and that may contain the price of major South African commodities such as platinum group metals and iron ore. On the other hand, Gold may benefit from the fog of global economic uncertainty or emerging geopolitical flashpoints, but its importance to the South African economy and its export profile is a fraction of what it once was. Should the global economy enter a deep recession in 2023 as expected by many analysts, the external performance and thus the Rand will be negatively affected.

Non-economic factors have also worked to affect South Africa’s performance on the external front.

LOGISTICS ISSUES: Transnet which is a fully owned South African Government organization operating as a corporate entity aimed at both supporting and contributing to the country’s freight logistics network continued to pose problems in achieving export performance with several strikes, inefficiency and corruption. It is estimated that there was an export loss of SAR 50 billion on an annualised basis last year for iron ore, coal, chrome, ferrochrome and manganese exporters, as measured by delivered tonnages against contracted rail tonnages. This compares to a loss of R35 billion in 2021 based on the same metric. Attempts to reform the system have failed repeatedly.

POLITICAL BOTLENECKS: The current President Mr. Cyril Ramaphosa, who had succeeded Mr. Zuma who was forced to resign amid numerous charges of corruption, however faced his own scandal. An independent report commissioned by the speaker of parliament said Mr Ramaphosa may have broken the law but he has denied any wrongdoing. After facing impeachment proceedings, he managed to survive a vote in Parliament. However, there are divisions within the party and his political future and hence the stability of politics in the country is under question. Preoccupations with political survival have affected economic performance.

DOMESTIC MACROS

On most parameters they performed better. GDP for Q3 2023 improved to 1.6% from -0.7% and bettered expectations also. Consumer Confidence rose from -20 to -8. As already mentioned earlier CPI inflation also came down. Manufacturing PMI rose to 50.6 from 49.5.

INFLATION AND RATES: In line with the global trend, recent inflation in South Africa also declined slightly and the Central Bank is likely to keep the monetary policy unchanged for now. From November 2021 to November 2022, they had raised its key repo rate by 350 basis points, bringing the prime lending rate to 10.5%. However, major global Central Banks are still on rate hike path as their inflation rate remains far higher than the target, hence the funds flow might get affected.

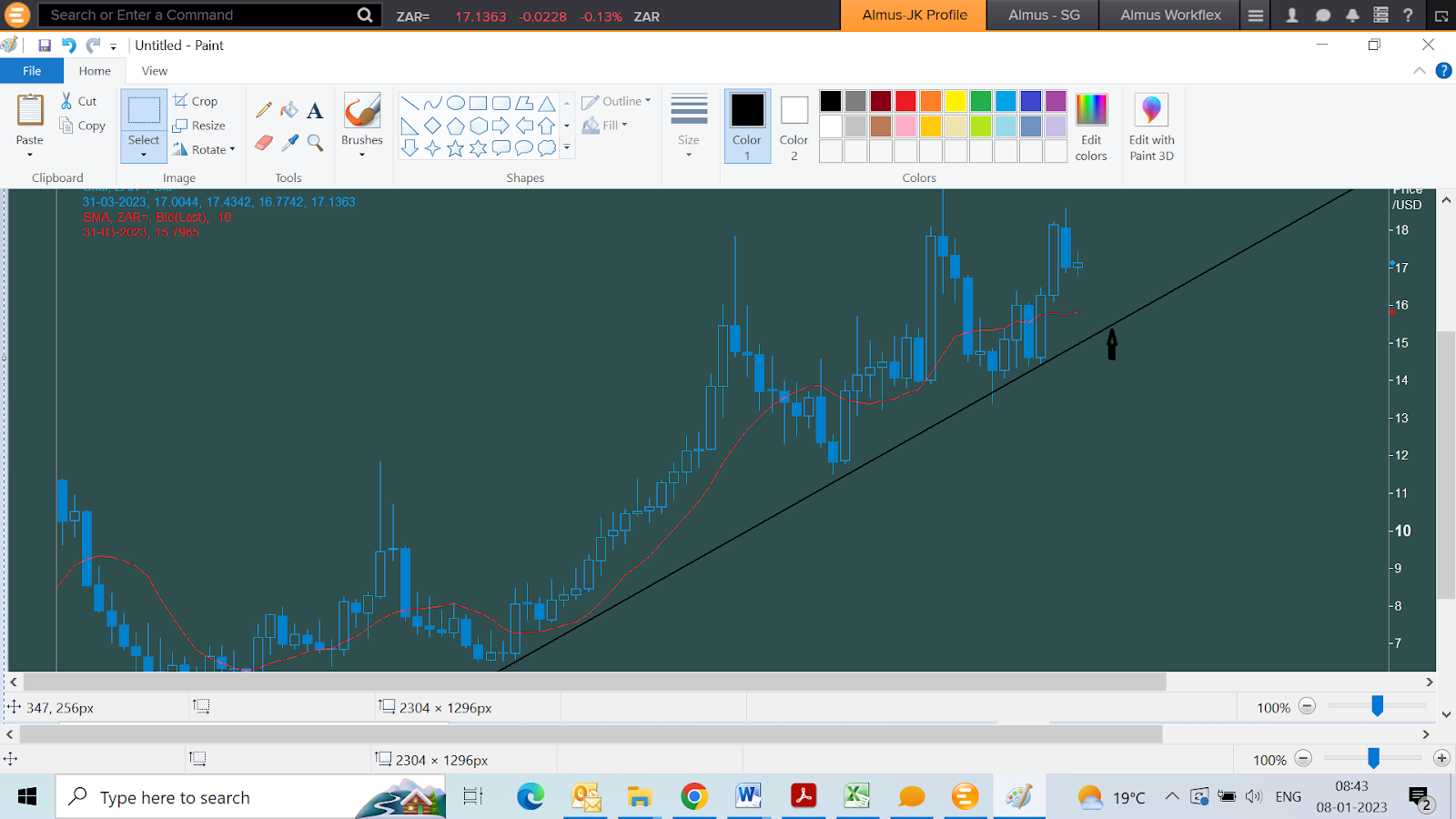

RECENT RAND MOVES AND OUTLOOK

Temporary resolution of political crisis, relative better performance on trade led by lower oil prices and also the fall in broader Dollar Index have helped Rand to perform better in the last two months. However, the structural problems haunting the economy remain and will keep it from gaining much. In fact, the latest fall in the Dollar Index has not seen Rand extend its gain much beyond 17.00 and has in fact weakened last week even as many EM currencies performed better.

Prospects of recession in major countries are likely to affect its exports and will keep the currency subdued.

TECHNICALLY, we continue to believe that the range of 16.50 to 18.00 will hold Rand moves at least in the first half of this year. Only a further large slippage in the broader Dollar can see more gains for the South African currency, but even then we do not expect 15.50 to break without a vast fundamental shift in its external performance.

SUPPORT LEVELS 16.60 AND 16.20

RESISTANCE LEVELS 17.30 AND 17.75