“Two roads diverged in a wood … I took the one less travelled by, and that has made all the difference.” – Robert Frost

The quote does talk about two roads diverging, but for few of the major central banks its just one with a question on timing of when to begin the journey on the road. 2024 looks set with a series of major events for the financial markets with numerous random & uncertain changes at fore, difficult to predict. Yet we tend to engage in this activity of outlining the probable outcomes. Quite interestingly it can definitely help provide a map to taking into consideration major narratives to traverse through this maze with some guidance in the background. Considering this following are the narratives expected to be at play for the next few months of 2024.

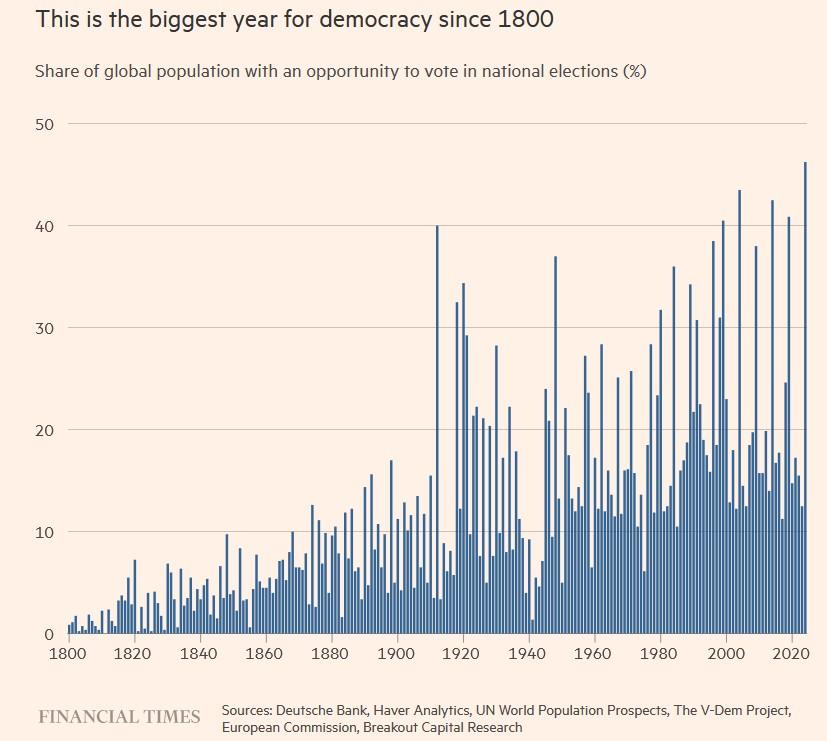

Democratic Abundance!

More than 30 democracies are scheduled for elections in 2024 with larger nations like India, US & Indonesia also contesting. Although discussions around stability of govt. and re-election of the incumbents for the Indian nation have gained prominence over the last couple of months, it’s the US elections which are seeing quite interesting set of developments. Volatility which was bit subdued during the end of 2023 should see some pick up in the current year with further more developments in the political landscape.

Central Bank Conundrum!

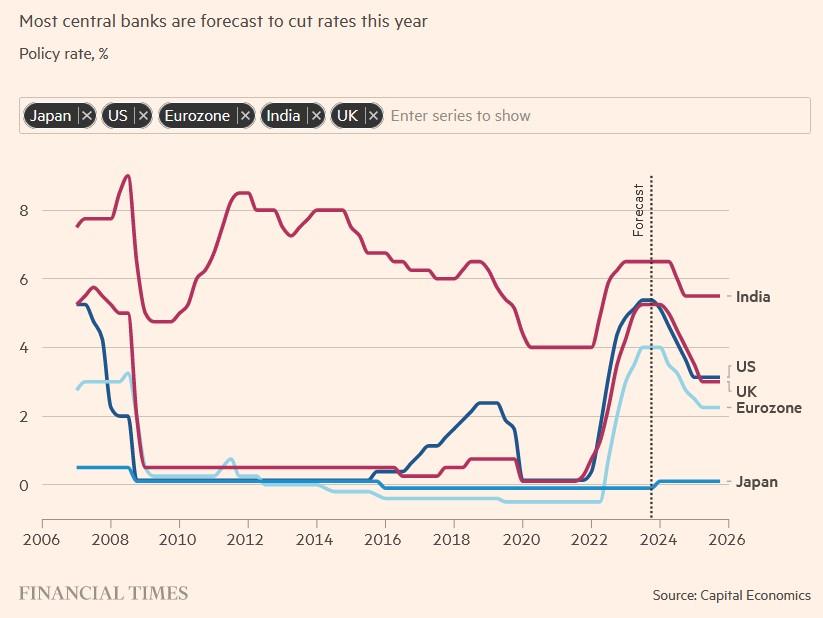

Steadily falling inflation and slowing economy has prompted FED to turn dovish on monetary policy and the dot plot indicates up to 0.75% rate cut in 2024. Since then, market expectation of rate cuts has risen to 1.5% this year. Rate cuts of this magnitude can happen only in case of a financial crisis or a big slump in the U.S. economy. What FED is trying to achieve is a soft-landing and avoid a recession in a crucial election year. At the same time, they would not like to ignite fresh rise in inflation by hefty rate cuts (unless necessitated by a crisis).

Central banks have repeatedly impressed on their dependency to data for their actions leading to participants closely following the labour markets, wage growth and the numerous variations of inflation indicators. Concerns around the impact of recent rate hikes not being seen thoroughly places attention towards the debt refinancing and maturity in the shorter term – to identify the possibility of further slowing of economy.

Though 20 major central banks are expected to cut rates this year according to economists – central banks still weary a repeat of 1970s i.e. cutting rates prematurely leading to second round of inflation – thereby keeping pace slower than expected.

The global financial markets would see a lot more of other factors like China performance, Euro zone recovery, Geo-politics and other thing – but it’s the policy & the politics which is expected to set the general trend for the year.

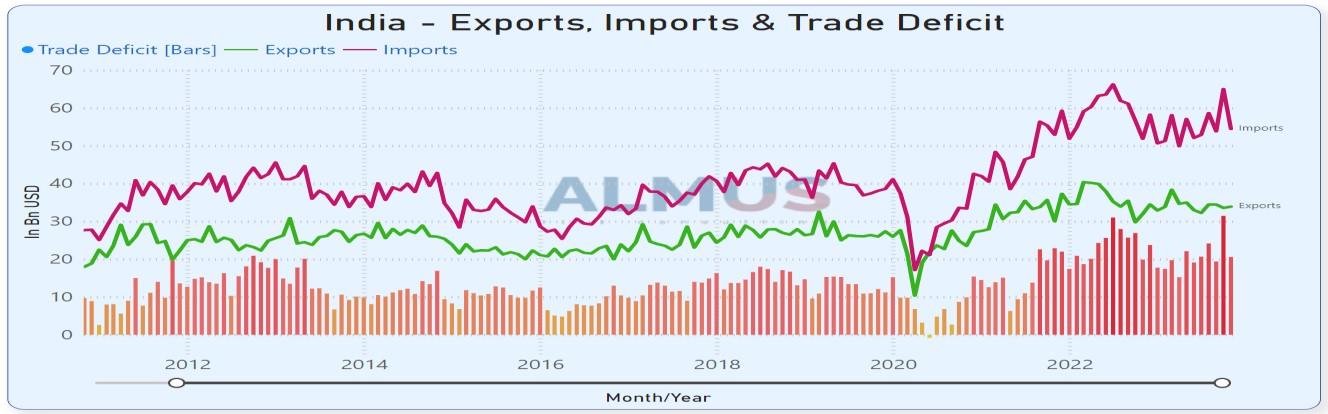

USDINR

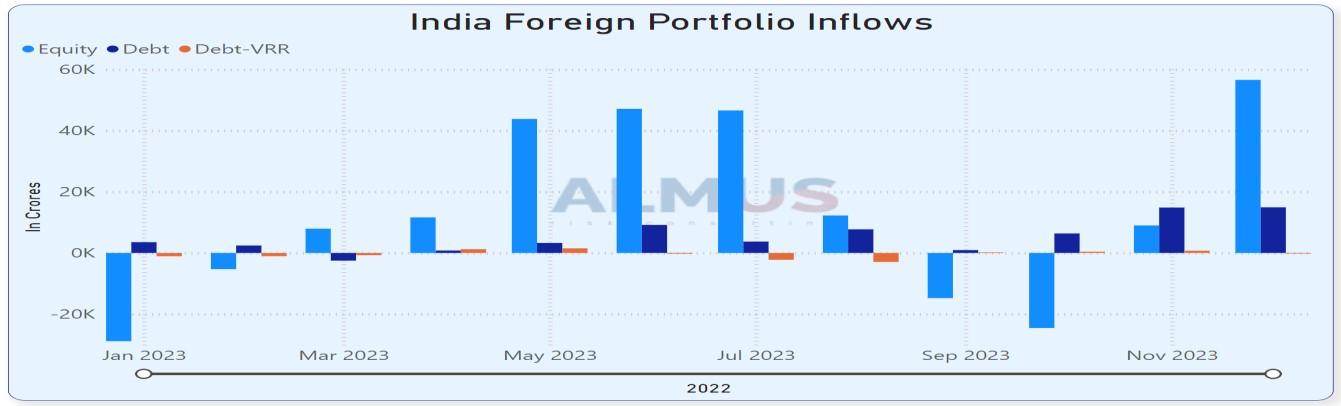

India was once assumed to be a key member of the ‘Fragile Five’ with many major banks terming it to be one of the vulnerable emerging economies. Recent discussion seems to have quite a distinguished view for the nation compared to the ones mentioned earlier. India has been one of the hotter destinations for the flows to have arrived along with consistent expectations of outgrowing global economies in terms of pace in the coming years.

Expect Rupee to perform better in first two quarters due to:

Huge inflows expected to the Bond market

Current expectation of stable Government returning to power in May likely to boost investments

FDIs – which have been underwhelming in 2023 is expected to pick up as India continues to grow faster and stable government attracts long term investors

Dollar Index is expected to be soft into the CY Q2 considering expectation of Fed Rate Cuts

Lower oil prices are expected to sustain which shall help keep the nations external deficits at manageable levels

Expect Rupee to weaken in second half of the year due to:

Dollar Index is expected to gain once FED cuts rates, but expect them to undershoot market expectations

India’s high growth will keep imports on the higher side and persistent deficits will necessitate keeping the Rupee weaker

RBI expected to cut rates in the second half of the year; this should weaken the Rupee

Indian assets are expected to see some correction with valuation concerns dominating

INR historically weakens 3 – 3.5 % p.a. on average in a longer-term horizon due to its structural deficit. This did not happen in 2023 due to RBI arresting it with inflation concerns. Although INR is expected to appreciate in the first two quarters, it’s the consistent imports, slowing economies revaluation of assets and dollar strength which may bring in depreciation for the Rupee by the end of calendar year.

TECHNICALLY, initial down move can see the Rupee hit Rs. 82.00 or Rs. 81.50 levels against the dollar.

The subsequent weakness can be expected to move it higher towards Rs. 84.50 levels towards year end.

Dollar Index

If the US economy does achieve a soft-landing while at the same time market expectation on rate cuts is moderated, it will support the Dollar by making investments in the U.S. assets attractive. As mentioned earlier – the U.S. goes through elections this year with a lot of uncertainty as to which political disposition will have the edge Given this background, expectation of the Dollar moves during the year- Dollar is expected to weaken further into the Fed rate cut beginning Slowing of the economy should further put pressure on the strength for dollar As their actual actions undershoot market expectations, can expect Dollar to regain strength later Lingering geopolitical uncertainty and continued strain in U.S. China relations will keep the global trade on uncertain footing. This will be supportive of the Dollar as a SAFE HAVEN Policy uncertainty due to upcoming elections in the U.S. will be detrimental to risk assets globally Thus, initial period of Dollar weakness should give way to Dollar strength in the second half of the year.

MEDIUM TERM: However, medium-term view of Dollar is one of more weakness due to (a) precarious fiscal situation in the U.S. which will eventually lead to a depreciation of the Dollar; (b) ongoing diversification or de-Dollarization of the Dollar is an underlying factor to keep the greenback weak.

TECHNICALLY, initial weakness will see the Dollar Index drop to 98.00 or slightly lower. However, after that it is expected to have a rebound to 105/107 levels. In other words, a drop in Dollar by another 4% from the current level of 103 should be followed by a strong corrective rebound. EURO Broadly Dollar moves are determined by the trends in EURO which has maximum weightage in the DXY. EURO has displayed distinct bullishness since the low of 0.9535 seen in September last year. It can be gauged from the fact that all through 2023 and till now, EURO Zone economy has underperformed the US counterpart and its yields have been lower than that of U.S. The largest Euro Zone economy, Germany has seen a technical recession while the Region as a whole has recorded a negative growth in Q3.

Euro has derived its strength from Central Bank diversification of reserves and also structural short position in the single currency being unwound. EURO’s gain of 1.6% on a YOY basis does not look significant, but its recovery of over 15% from the multi-year low speaks of the massive short-covering that investors have done.

Another factor supporting the Euro has been that while the FED has gotten dovish recently, ECB still remains glued to HIGHER FOR LONGER rates notwithstanding the weak growth picture. However, this is likely to change in the coming months as inflation in the Euro Zone has been falling faster and it is a matter of time ECB turns dovish too. In fact, markets have been discounting over 1% rate cut during the year for EURO starting in the second quarter of 2024. Once the ECB starts to align with the market, EURO reversing some of its gains can be expected. Elections in some of the member countries, viz. Austria, Belgium and Portugal, even as political set up in other countries are not very strong can bring in some volatility. Even the European Parliament is set for elections this June.

TECHNICALLY, EURO has an upside potential to 1.1250 or even 1.1500, before it retraces towards 1.05 in correction. However, medium term outlook for EURO is strong.

Sterling Pound/GBP:

Just like the EURO, UK Pound benefitted from the market’s structural short position being unwound and it posted even better grain of 3.5% on YOY basis. The massive short position in Pound was the reason why market ignored the weak performance by the economy, although the big rise in interest rates and the restoration of fiscal credibility were reasons too. Recently, inflation in UK also dropped quite heavily (from peak of 11.1% in October 2022 to 3.9% in November 2023), after which slightly dovish voices from the Bank of England members were heard. Market expects the Central Bank of UK to start cutting rates in Q2 of this year, though the Bank continues to push against such expectations.

UK also goes into general elections in next one year, although Prime Minister Rishi Sunak is not obliged to call an election until 17 December 2024, exactly five years since the last one took place. After many years, the incumbent Government has to deal with many issues like rising cost of living, high inflation and record interest rates, while the latest data shows GDP contracting in Q3.

Given this background, UK Pound is in for a period of underperformance both against the USD and the EURO in the coming year, though it will generally track the fortunes of the broader Dollar.

Technically, Pound will find it difficult to gain beyond 1.32 this year, while subsequently a drop towards 1.20 is not ruled out tracking the Dollar strength.

The Japanese Yen

Yen is likely to strengthen in the year due to- FED’s dovish posture resulting in rate cuts; gradual reversal of easy money policy by the Japanese Central Bank; Unwind of carry trades as other Central Banks like ECB and BOE cut rates later in the year; Japanese markets possibly outperforming an attracting foreign funds into the country Monetary policy change in Japan is overdue as their inflation has stayed well above target for long and expected to inch up further as wage revisions take place. BOJ has also linked their policy change to rise in wages.

Technically, dip towards 136.70 or even 133.70 appears likely as in a large correction to an uptrend. The quarterly chart’s structure suggests that a dip to 130.75 is also not ruled out. Resistance near 149/153 to cap any upside attempts by USDJPY.

The Chinese Yuan

Chinese Yuan was a stark underperformer in 2023, weakening as much as 5.5% against the USD. Main drivers were the widening rate differentials with the U.S. (FED raising rates and China cutting rates), sharply weakened Chinese Economy, large outflows from investors and fall in their exports on YOY basis by 2.5%. However, due to persistent efforts of Chinese authorities, weakness into new lows was averted and the currency recovered towards close of the year with some green shoots observed in the economy. Although China’s equity composite index probed new lows in the beginning of 2024.

Outlook for the Chinese economy is better for 2024 as lagged effect of various policy moves and supports start to reflect. Barring a slump in global trade, worsening of their relations with the U.S. and geopolitics China should see better year and that will be seen in the currency as well.

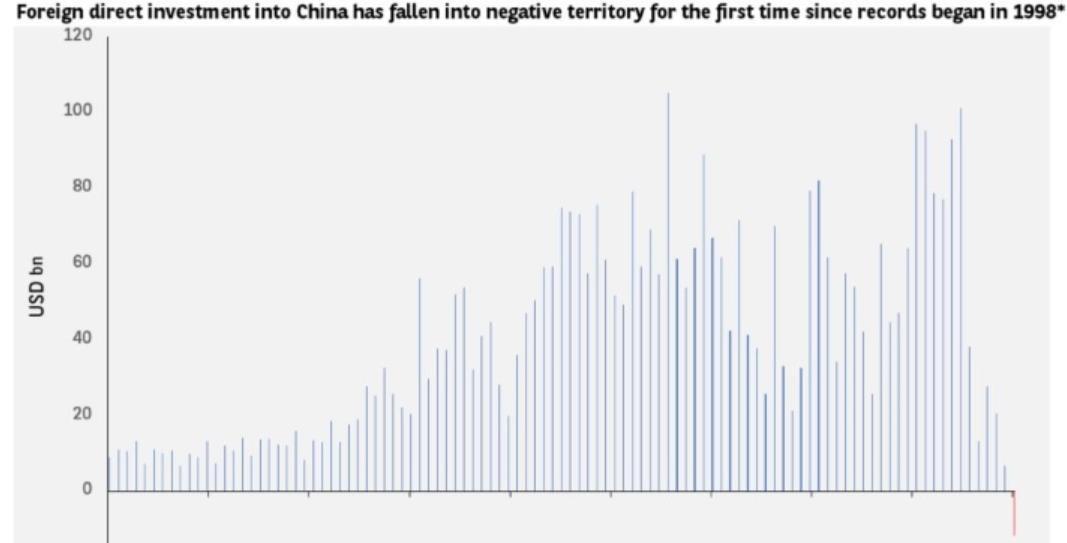

One alternate scenario for China cannot be ruled out. As we all know, China disappointed with its recovery vis-à-vis expectations post Covid relaxations. Despite the many measures taken by the Government/Central Bank, the economy and the markets have failed to respond positively. Following points are notable- Chinese Shanghai Composite is near Covid lows in stark contrast to global composite Index which has almost doubled FDI into China fell into negative territory last year for the first time since records began in 1998 Chinese Yuan fall of over 7% matched that of the Yen which carries negative policy rate whereas the DXY itself was lower by nearly 2%.

The problems in Chinese economy are structural in nature rather than being cyclical. Hence, it is another probable situation that China may adopt a bold move to cut their rates big and allow the Chinese Yuan to fall (which they have been resisting so far). In such case, Yuan can fall to 7.50 or more against the USD.

Technically, charts show that the underlying uptrend could undergo a correction by dipping towards 7.02 (minimum) or even to 6.85 area in the coming 6 to 12 months’ period. Resistance is near 7.22/7.28 and a farther one at 7.34/7.37. Rise above 7.37 shall bring in another round of weakness for the CNH against the dollar.

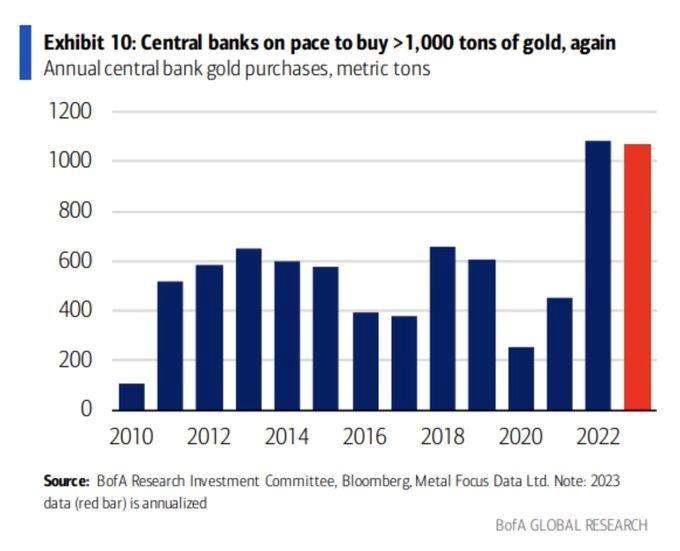

GOLD

The precious metal has performed strongly in 2023 rising 7% on YOY basis, helped by falling inflation rates across economies, policy rates expected to be slashed by the FED, consistent Central Bank accumulation of gold and Dollar diversification. This trend is likely to continue into 2024 as other major Central Banks in UK and Europe get dovish and cut rates. The structural weakness of USD due to their extremely weak fiscal position adds to attraction of gold. Further compression in real yield would further boost the overall attractiveness for the yellow metal.

Technically, charts continue to appear bullish for a rise to 2250. Supports are near 1980/1970 and a deeper one is at 1920. Fall below 1920 would lessen the chances for the expected rise. Sustained break above 2080 USD means that gold has ended its 12-year consolidation phase (1920 was seen in September 2011) and coupled with break of FOUR TOPS AT 2070-80 RANGE could lead to big gains for the metal.

Conclusion: To sum things up – Geo-politics shall play a important role in adding uncertainty to the financial markets this year. Central banks would try sail the ship through this uncertainty of geo-politics, historically instances of another round of inflation, slowing economy and heavy fiscal situations.

The expectations mentioned in the report are expected to help navigate in the next couple of quarters with further guidelines & directions to be evaluated over time.

Prepared by:

Mr. Jayaram Krishnamurthy,

Co-Founder and COO – Almus Risk Consulting LLP

Mr. Shikhar Garg,

VP – Treasury Markets – Almus Risk Consulting LLP