Time is your friend; impulse is your enemy – Jack Bogle

Just what the first month of the calendar year tested as it was less eventful for the markets than it usually is without hinting emergence of any new direction. Still abundant liquidity, fluctuating data points from major economies, uncertain geopolitical situation and Central Bank guidance were the focus of investors and traders trying to discern a sustainable trend. The major themes that guided the markets were:

- Inflation seemed to be attaining some stickiness and maintained a gap with the target rate which Central Banks were not comfortable with

- All the major Central Banks had their policy meeting and maintained status quo as expected

- No major theme emerged from the yearly Davos meet in Switzerland where the elite politicians/businessmen/analysts met

- Forward guidance from the policymakers continued to push back against market’s overly optimistic expectation on rate cuts

- A good number of countries are going into elections this year which kept the analysts busy assessing the prospects. Taiwan elections saw the existing regime continuing.

- The outperformance of the U.S. economy, now termed as U.S. EXCEPTIONALISM, continued while Europe did not show any decisive turn for the better

- China has continued to be the laggard even with big policy move and their largest real estate company Evergrande was directed to liquidate by the Hong Kong court

- Geopolitical situation in the Middle East neither escalated majorly nor showed any signs of ending. Attacks continued from both sides in the Red Sea affecting ship movements, but did not affect the markets significantly including oil.

- Indian Government presented interim budget which continued to focus on strong growth while maintaining fiscal prudence and imposed no fresh tax burdens either direct or indirect. Due to elections, the detailed budget will be presented after the new Government assumes office. Markets received the Vote on Account very positively.

- EMs continued to be at various stages of monetary policy – Turkey hiked policy rate by 2.5% (their eight hike in as many months) to 45%, taking total hikes since June 23 to 36.5% (their inflation rate is 65%); On the other hand Brazil cut their policy rate by 0.5%, their fifth reduction since July 2023. Rates have fallen from 13.75% to 11.25% in this period. Other EMs maintained their policy rates unchanged.

| U.S.A | EUROPE | U.K. | JAPAN | CHINA | INDIA | |

| Particulars | current vs. prev | current vs. previous | current vs. prev. | current vs. prev. | current vs. prev. | current vs. prev. |

| GDP QOQ | 3.3% vs. 4.9% | 0% vs -0.1% | *-0.1% vs. 0 | *-0.7% vs. -0.5% | 1% vs 1.5% | 7.6% vs. 7.8% |

| Ind. Prod YOY | 1% vs. -0.6% | -6.8% vs -6.6% | *-0.1% vs. -0.5% | *-0.7 vs -1.4 | 6.8% vs. 6.6% | 2.4% vs. 11.6% |

| PMI MFG | 50.3 vs. 47.9 | 46.6 vs. 44.4 | 47.3 vs. 46.2 | 48.1 vs. 48.7 | 49.2 vs. 49 | 56.9 vs 54.9 |

| PMI SERV | 52.9 vs. 51.4 | 48.4 vs. 48.8 | 53.8 vs. 53.4 | 51.5 vs. 50.8 | 50.7 vs. 50.4 | 61.2 vs 59 |

| Jobless Rate | 3.7 vs. 3.7 | 6.4 vs. 6.4 | 4.2 vs. 4.2 | 2.4% vs. 2.5% | 5% vs. 5% | 10.5 vs. 7.09 |

| Inflation | ||||||

| Headline | 3.4% vs. 3.1% | 2.8% vs. 2.9% | 4.0% vs. 3.9% | 2.6% vs. 2.8% | -0.3 vs -0.5 | 5.69 vs 5.55 |

| Core | 3.9% vs. 4% | 3.3% vs. 3.4% | 5.1% vs. 5.1% | 2.3% vs. 2.5% | 0.6 vs 0.8 | 3.89% vs 4.1% |

| Consumer Confidence | 114.8 vs 108 | *-16.1 vs. -15.1 | *-22 vs. -24 | 38 vs. 37.2 | 87 VS. 87.9 | 92.2 vs. 88.1 |

| Leading Eco.Index | -0.1 vs. -0.5 | *-0.8 vs. -1.1% | *-0.5% vs. -0.4% | 107.6 vs 108.9 | *-0.1 vs -0.3 | |

| POLICY RATE | 5.25% – 5.50% | 4.50% | 5.25% | -0.10% | 3.45% | 6.50% |

In the U.S. Consumer Confidence surged strongly, but the forward looking Leading Economic Index of the Conference Board continued to drop. The Board expects GDP growth to turn negative in Q2 and Q3 of 2024 but begin to recover late in the year. But with inflation remaining sticky and job market continuing to be strong (unemployment rate low and wages rising strongly) FED Chairman Powell said that they need more confidence on inflation sustainably falling to target of 2% before they dialled back high interest rates. FED is also likely to discuss lowering their quantitative tightening programme in the meeting in May. ECB and BOE also remained noncommittal on rate cut timing although they also agree that the next move will be a cut. Markets expect rate cuts to start in all three in the second quarter of 2024.

China made a big move to stimulate the economy by cutting the Reserve Rate Requirement by 1% which released 1 trillion Yuan of additional liquidity to the system. However, the effect of the same on the market was temporary. China requires more structural reforms to lift the economy. As far as Japan, consensus is that they will move out of negative rate of interest in April. They have linked monetary policy change to wage hikes which are likely to be substantial.

IMF’S WORLD ECONOMIC REPORT JANUARY, 2024

IMF raised forecast for global economic growth to 3.1% in 2024 vs. 2.9% in October, keeps 2025 outlook unchanged at 3.2% and forecast global headline inflation to be unchanged at 5.8% in 2024, lowers 2025 forecast to 4.4% vs. 4.6%. US Growth has been upgraded to 2.1% in 2024 vs. earlier 1.5%, but for Europe revised down to 0.9% from earlier 1.2%. It lifted China GDP forecast to 4.6% in 2024 vs. 4.2% in October; leaves 2025 forecast unchanged at 4.1%

IMF said global economy displaying ‘remarkable resilience,’ on final descent toward ‘soft landing’ while trade frictions, geo-economic fragmentation could weigh on growth.

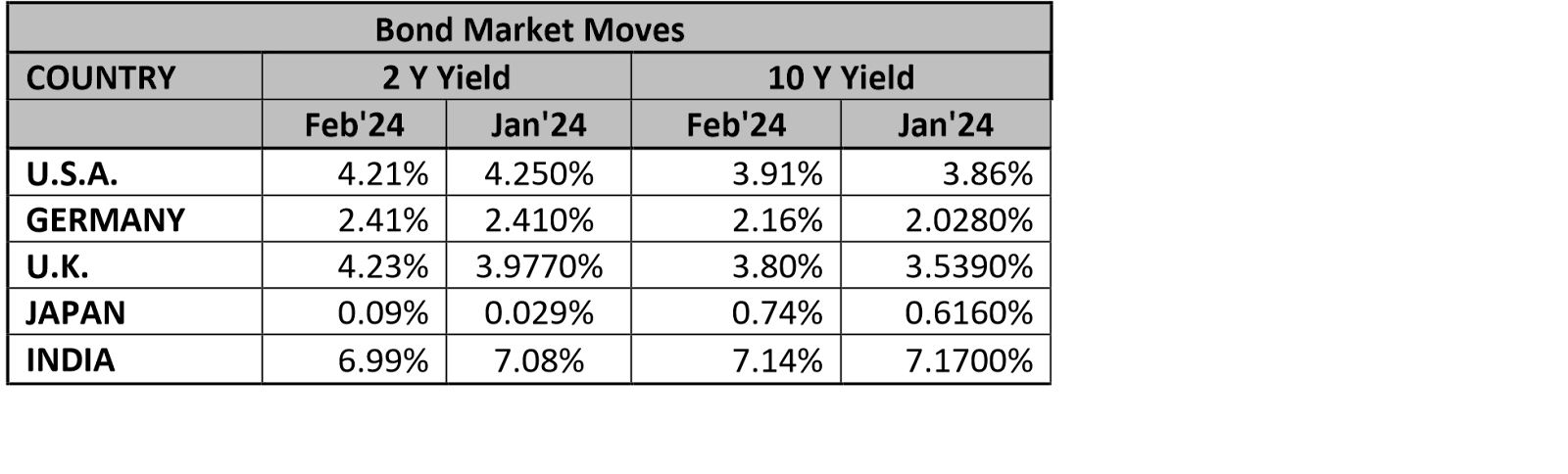

BOND MARKET:

Bond yields have been quite volatile, but within a range. Interestingly, US yields which retraced higher in early part of the month based on steadier inflation and strong jobs report, later continued to fall notwithstanding impressive GDP growth and other improved indicators. Direction of Yields in other major countries shadowed that in US, while Japanese yields were steadily higher on expectation of a policy change.

Bond yields in India for 10 year have since moved lower by 10 basis points to 7.04, after the Government submitted interim budget for FY25 where they projected much lower fiscal deficit target of 5.1% vs. 5.8% for FY24. Total borrowings are expected to be well manageable, particularly as we are entering an era of lower interest rates starting quarter 2 of this year.

Equity Markets

Equity markets have chugged along in the month of January as liquidity was still the main driver with investors looking more at the outperformance of the US Economy and Europe showing tentative signs of recovery. The other positive factor was the expectation of rate cuts between 1% and 1.5% from the BIG THREE Central Banks.

| Indices | 31st Jan 2024 | 31st Dec 2023 | Abs Change | % Change |

| Dow Jones | 38,150 | 37,689 | 461 | 1.22 |

| S&P 500 | 4,848 | 4,769 | 79 | 1.66 |

| Nasdaq | 15,164 | 15,011 | 153 | 1.02 |

| German DAX | 16,903 | 16,751 | 152 | 0.91 |

| UK FTSE | 7,630 | 7,733 | -103 | -1.33 |

| China Composite | 2,788 | 2,974 | -186 | -6.25 |

| Japan Nikkie | 36,286 | 33,464 | 2,822 | 8.43 |

| India Nifty 50 | 21,725 | 21,731 | -6 | -0.03 |

As can be seen, Japan and China had extremely contrasting performance, the former hitting new 40 year high and attracting fresh investors due to its attractive valuation while the Chinese Composite Index could not sustain any recovery despite the 1% RRR cut by the Central Bank. Investors are looking for stronger measures by the Chinese authorities.

India had a rare underperformance during the month ending almost unchanged from previous month. Technically, it has formed a DOJI candle at the multi-year top and after rising almost 200% from its Covid Lows. Just for a comparison, the Chinese Market still languishing near the Covid lows.

The expectations are not very bullish on stocks going forward in the year 2024 due to

- valuation concerns;

- liquidity reduction as CBs continue quantitative tightening;

- Lagged effect of hefty rate hikes impact companies’ performance and possible slowing of U.S. economy.

Currency Markets

Dollar recouped part of its losses of December as market looked oversold and moved higher along with recovery in yields. Once again, Japanese currency weakened more due to its widened yield difference. However, in the latter part of the month, it was seen the Dollar was moving in a narrower range with uncertainty about the timing and extent of rate kept moving. It was also not surprising to see the Chinese Yuan resume its weakness as market continues to see outflows and Chinese assets are not finding any sustainable interest. Weakness in the Chinese Yuan also kept the Asian currencies on the weaker.

| Currency | 31st Jan 2024 | 31st Dec 2023 | Abs Change | % Change |

| USD Index | 103.27 | 101.38 | 1.89 | 1.83 |

| EURUSD | 1.0816 | 1.1037 | -0.0221 | -2.04 |

| GBPUSD | 1.2685 | 1.2732 | -0.0047 | -0.37 |

| USDJPY | 146.88 | 141.04 | 5.84 | 3.98 |

| USDCNH | 7.1849 | 7.1252 | 0.0597 | 0.83 |

| USDINR | 83.095 | 83.24 | -0.145 | -0.17 |

A rare outperformance by the Indian Rupee with Dollar being on the losing side, albeit by a small percentage. Rupee was stronger despite net outflows from FIIs to the extent of USD 1 bio in January. While there were large outflows from FIIs for stocks, it was largely offset by inflows for Bonds and other fund raising by corporate through Bonds as well as ECBs. It was also noticeable that RBI was less active in the market.

Key themes/market drivers in India –

- Positive vibes after the state election results were carried into the month of January, helping the market to hold on to its highs

- India’s merchandise trade deficit narrowed to below USD 20 bio once again, with rise in imports being offset by good increase in exports

- Indian Government presented its interim budget for FY 25 with continued emphasis on infrastructure investment that helps higher growth and employment, important socioeconomic measures important for a diverse country like India, proposed no changes to the taxation rates (both direct and indirect) and planned to reduce fiscal deficit by 0.7% for FY25

- Lower fiscal deficit will be taken by the global investors very positively and more importantly, global ratings agencies may even look at upgrading us

- The huge positive of the budget has helped the markets to rally strongly. Key stock indices touched their all-time high while bond yields dropped due to comfortable borrowing programme

- For the first time, S&P published flash PMIs for India showing both manufacturing and services picking up further momentum and placed India at the top of the pack as far as economic activity growth is concerned.

Outlook : Global

IMF expects country to grow by 6.7% from earlier projection of 6.3%. For FY25 and FY26, India’s GDP growth is seen steady at 6.5%, a 20 basis point upgrade from its October 2023 forecast, the IMF said in its latest report released. Of course, at 6.7% GDP growth forecast for India in FY24, the IMF’s forecast is lower than both the Reserve Bank of India’s 7% estimate and the National Statistics Organisation’s (NSO) first advance forecast of 7.3% for the financial year ending March 2024.

The blockbuster jobs report for January from US has re-established resiliency of the economy even in the face of high interest rates. As a result bond yields had risen and so did the Dollar through key resistance. The question before investors is whether the FED will change their earlier plans of cutting rates by 0.75% this year due to the upbeat picture of the economy (both GDP and employment). That will be answered in the days to come when there’s more data on inflation. Expectations are that FED will cut rates if inflation stays subdued as high rates are eventually likely to affect growth. Near term we look for the Dollar to recover based on attractive yields and also positioning of the market which seems to be heavily short on the Dollar.

However, in medium term expectations are for the Dollar to weaken quite substantially as the fiscal and debt issues will be a macro headwind. As per data, foreigner holding of US Securities is steadily declining and this means authorities will have to weaken the Dollar eventually to attract capital.

We expect Dollar Index to move between 103 and 105.50 during the month.

Looking at the various macro developments in our economy, one would be tempted to call it INDIAN EXCEPTIONALISM. High growth, fiscal prudence, moderating external balances and strong flows from global investors puts India on a different plane which is already reflected in a super-strong performance of the equities.

Inclusion of Indian Bonds in major EM Bond indices was a big recognition of India’s place, but an upgrade by the global rating agencies may be due as well.

Expect a period of outperformance by the INR in the coming weeks/months as much of the good news is not in the current levels and as flows rise steadily, a stronger rally is on the cards.

USDINR should remain range bound between 82.50 to 83.40 in the current month, but can expand on downside after the current bout of up move in the Dollar Index ends.

Technical Outlook

The ranged action for the currency pair continues although there has been a slight increase in the daily range. Several attempts at breaking the 82.80/82.90 support zone for USDINR has been seen, break of which should provide further downside action in the pair towards 82.50 although speculative buying, public sector bank buying and importer purchasers have kept the rupee appreciation limited. Upside looks well protected around 83.20 initially and then 83.40/45 levels.

Commodity Outlook (Gold)

GOLD: COMEX: XAUUSD: CMP: USD 2021

Attempts at breaking above the USD 2070/2080 range have been numerous but the sustenance of the prices above has been questionable by far. Although the metal is bullish in it’s underlying trend over the 3-6 month horizon the prices action has been of consolidation in the past couple of weeks. The precious metal is expected to move upwards as conviction of rate cuts during the year by FED increases and real yields decreases. Targets in the longer term stay at USD 2200/2300 levels initially. Supports around USD 2005 initially and later at USD 1970 for the month can be observed break of which the metal can again set into a consolidating move for some more month.

The yellow metal against INR on MCX also moved sideways in the previous month with bias for bullish action while USDINR component keeping volatility limited. The charts suggest a channel break is required for significant action on the upside thereby putting initial resistances around INR 63250 and INR 64150. Break above these levels shall bring in bullish action targeting INR 67500 above.

Supports around INR 62000 and INR 60300 should hold any downside push during this bullish rally expectations.

Prepared by:

Mr. Jayaram Krishnamurthy,

Co-Founder and COO – Almus Risk Consulting LLP

Mr. Shikhar Garg,

VP – Treasury Markets – Almus Risk Consulting LLP